Page 84 - UBF AR 2018 - E Version

P. 84

NOTES TO THE FINANCIAL STATEMENTS

Year ended 31 March 2018

32.4 Assets and liabilities measured at fair value - fair value hierarchy

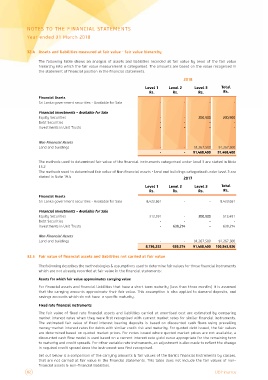

The following table shows an analysis of assets and liabilities recorded at fair value by level of the fair value

hierarchy into which the fair value measurement is categorised. The amounts are based on the value recognised in

the statement of financial position in the financial statements.

2018

Financial Assets Level 1 Level 2 Level 3 Total

Sri Lanka government securities - Available for Sale Rs. Rs. Rs. Rs.

- - - -

Financial Investments – Available for Sale

Equity Securities - - 200,900 200,900

Debt Securities

Investments in Unit Trusts -- --

-- --

Non Financial Assets - - 91,267,500 91,267,500

Land and buildings - - 91,468,400 91,468,400

The methods used to determined fair value of the financial instruments categorised under level 3 are stated in Note

15.2

The methods used to determined fair value of Non financial assets - land and buildings categorized under level 3 are

stated in Note 19.4 2017

Financial Assets Level 1 Level 2 Level 3 Total

Sri Lanka government securities - Available for Sale Rs. Rs. Rs. Rs.

- -

Financial Investments – Available for Sale 8,423,661 8,423,661

Equity Securities

Debt Securities 312,591 - 200,900 513,491

Investments in Unit Trusts - - - -

- 639,274 -

Non Financial Assets 639,274

Land and buildings

- - 91,267,500 91,267,500

8,736,252 639,274 91,468,400 100,843,926

32.5 Fair value of financial assets and liabilities not carried at fair value

The following describes the methodologies & assumptions used to determine fair values for those financial instruments

which are not already recorded at fair value in the financial statements:

Assets for which fair value approximates carrying value

For financial assets and financial liabilities that have a short term maturity (less than three months) it is assumed

that the carrying amounts approximate their fair value. This assumption is also applied to demand deposits, and

savings accounts which do not have a specific maturity.

Fixed rate financial instruments

The fair value of fixed rate financial assets and liabilities carried at amortised cost are estimated by comparing

market interest rates when they were first recognised with current market rates for similar financial instruments.

The estimated fair value of fixed interest bearing deposits is based on discounted cash flows using prevailing

money–market interest rates for debts with similar credit risk and maturity. For quoted debt issued, the fair values

are determined based on quoted market prices. For notes issued where quoted market prices are not available, a

discounted cash flow model is used based on a current interest rate yield curve appropriate for the remaining term

to maturity and credit spreads. For other variable rate instruments, an adjustment is also made to reflect the change

in required credit spread since the instrument was first recognised.

S et out be low is a c ompariso n of the carrying amounts & fair values of the Bank’s financial instruments by classes,

that are not carried at fair value in the financial statements. This table does not include the fair values of non–

financial assets & non–financial liabilities.

82 UB Finance