Page 80 - UBF AR 2018 - E Version

P. 80

NOTES TO THE FINANCIAL STATEMENTS

Year ended 31 March 2018

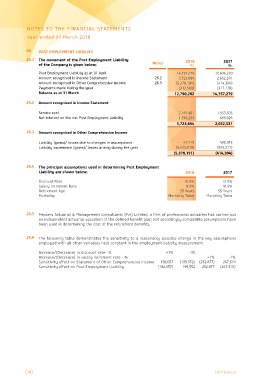

26 POST EMPLOYMENT LIABILITY Notes 2018 2017

26.1 The movement of the Post Employment Liability

26.2 Rs. Rs.

of the Company is given below; 26.3

14,757,279 12,836,230

Post Employment Liability as at 01 April 3,723,694 2,652,531

Amount recognised in Income Statement (414,304)

Amount recognised in Other Comprehensive Income (5,378,191) (317,178)

Payments made during the year (312,500)

Balance as at 31 March 14,757,279

12,790,282

26.2 Amount recognised in Income Statement 1,953,505

2,187,461 699,026

Service cost 1,536,233

Net interest on the net Post Employment Liability 2,652,531

3,723,694

26.3 Amount recognised in Other Comprehensive Income 408,913

47,719 (823,217)

Liability (gains)/ losses due to changes in assumptions (5,425,910) (414,304)

Liability experience (gains)/ losses arising during the year

(5,378,191) 2017

26.4 The principal assumptions used in determining Post Employment 2018 12.9%

Liability are shown below; 10.5%

10.0% 55 Years

Discount Rate 9.0% Mortality Table

Salary Increment Rate

Retirement Age 55 Years

Mortality Mortality Table

26.5 Messers Actuarial & Management Consultants (Pvt) Limited, a firm of professional actuaries has carried out

an independent actuarial valuation of the defined benefit plan and accordingly compatible assumptions have

been used in determining the cost of the retirement benefits.

26.6 The following table demonstrates the sensitivity to a reasonably possible change in the key assumptions

employed with all other variables held constant in the employment liability measurement.

Increase/(Decrease) in discount rate- % +1% -1%

Increase/(Decrease) in salary increment rate - % +1% -1%

Sensitivity effect on Statement of Other Comprehensive Income 192,057 (199,552) (252,877) 247,510

Sensitivity effect on Post Employment Liability (192,057) 199,552 252,877 (247,510)

78 UB Finance